Basel 4 Output Floor Calculation

Basel 4 Unfolds The Regulatory Challenges Continue Is Credit Risk Escaping Supervision The How And When 5 5 Treasury Insights Current Topics

Basel Iv How Close Are The Irba Banks To The Output Floor

Basel Iii S Final Reforms Explanation In A Nutshell Triple A Risk Finance

Basel 4 And The Reduction In Rwa Variability Capital Buffers And Capital Erosion Prometeia

Https Www2 Deloitte Com Content Dam Deloitte My Documents Risk My Ra Basel Iv Placemat Pdf

Output Floor Leverage Ratio And Other Regulatory Requirements Springerlink

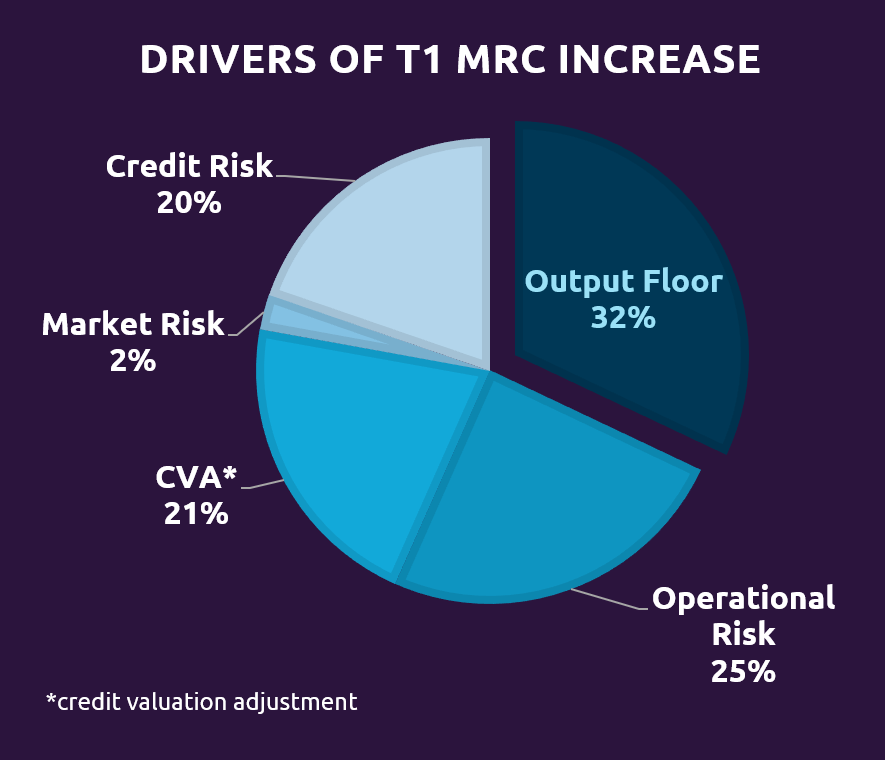

The output floor is designed to reduce inconsistency in rwas not justified by risk.

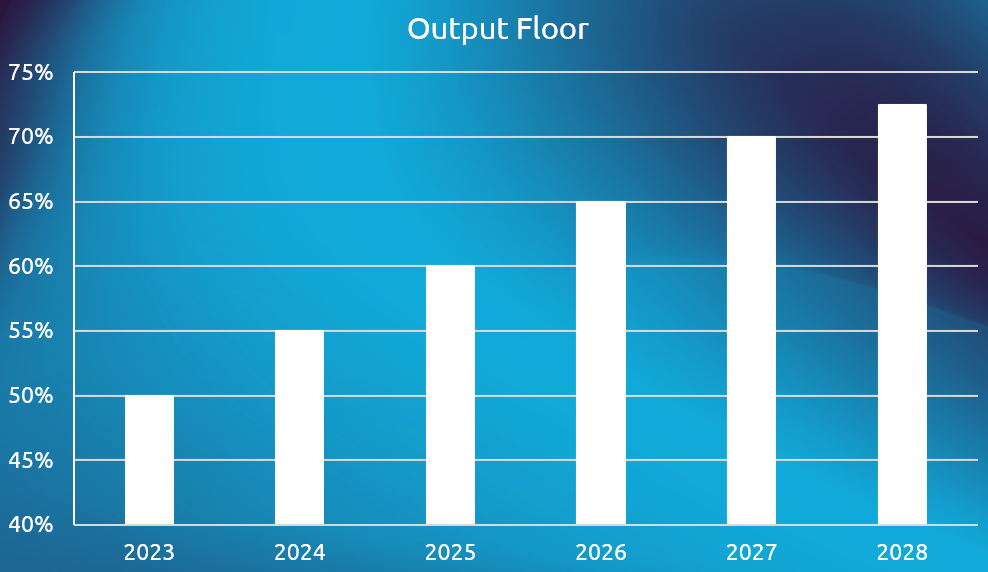

Basel 4 output floor calculation. This can also be extended to cover the combined impact across risk types credit market and operational. The changes will occur over a transitional period from 2022 2027 basel iii basel iv. Based approaches to the calculation of risk weighted assets for credit risk. The basel framework describes how to calculate rwa for credit risk market risk and operational risk.

The final agreement introduces an output capital floor one of the key elements of the negotiations. And the application of a capital floor to limit. Basel 4 nears completion. The use of this alternative is subject to supervisory approval.

The standardised approaches to be used to calculate the base of the output floor referenced in rbc20 4 2 are as follows. The eba has published a number of regulatory documents. The output floor ensures that banks capital requirements do not fall below a certain percentage of capital requirements derived under standardised approaches. The basel committee may also.

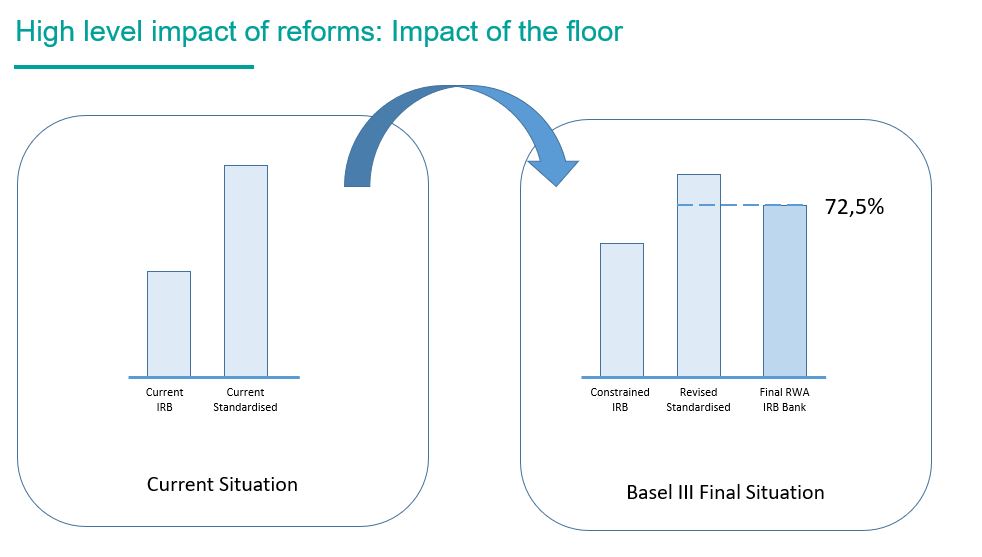

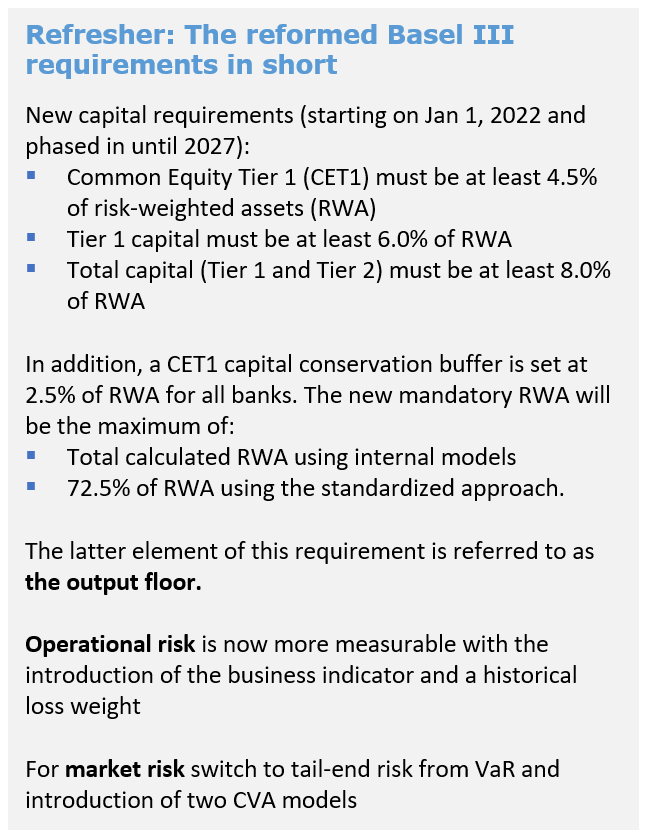

Banks calculations of rwas generated by internal models cannot in aggregate fall below 72 5 of the risk weighted assets computed by the standardised approaches. Use of the irb approach the output floor and the revised standardised approach and to assess corresponding business decisions. Finalization of basel iii. In december 2017 after many months of stalled negotiations the basel committee on banking supervision bcbs announced an agreement to complete the finalized basel iii rules also known as basel iv.

Optimal responses will vary by bank. Kpmg member firms have developed the basel 4 calculator as. Basel 4 nears completion. For example banks with focused business models could face a significant irb output floor requirement.

Non modelling approach must be updated to reflect the prevailing basel capital standards in force at the time of the floor calculation. 3 1 interaction of the output floor with other prudential requirements 21 3 2 calculation of rwas at granular level 27 3 3 scope of application of the output floor 29 3 4 role of provisions in the calculation of the output floor 33 3 5 transitional measures regarding the output floor 37 annexes 42 annex 1. Robust risk sensitive output floor based on the revised standardised approaches. 4 as indicated the standards for the output floor which would replace the transitional capital floor adopted in basel i are still being discussed.

Changes to internal models introduced by the basel committee the eba and the ecb. One of the key components of the basel iv package is the output floor which sets a floor in capital requirements calculated under internal models at 72 5 of those required under standardised approaches for calculating capital requirements for all pillar 1 risks.

Dutch Banks Basel Worries May Return As Regulator Mulls Early Adoption S P Global Market Intelligence

Finalyse Com Readiness For Basel Iv From A Bank S Perspective Finalyse

Https Eba Europa Eu Documents 10180 2886865 Policy Advice On Basel Iii Reforms Output Floor Pdf

Basel Iv Is Still Worthwhile To Use The Irba

Https Www Bbvaresearch Com Wp Content Uploads 2017 12 Watch Basel Iv Pdf

Box E Reforms To The Basel Iii Capital Framework Financial Stability Review April 2018 Rba

Saccr Vs Cem For Fx Products

Northern European Banks Confident Basel Iv Will Not Bring Capital Blow S P Global Market Intelligence

Dutch Banks Unflustered By Front Loading Of Capital Rules S P Global Market Intelligence

Basel Iv Is Here Pwc Has Produced Four Hot Topics On Each Of The Key Components Of The Basel Iv Package

Dutch Banks To Face Reduced Yet Still Significant Hit From Basel Iii S P Global Market Intelligence

Basel Iv What Influence Do Pd Lgd Input Floors Have On Rwas

Basel Iii Reforms What Will Impact Banks Most